Infrastructure spend will help construction’s post-covid recovery, but is a rapid bounce back likely? Kris Hudson examines the data.

The UK economy saw its fastest contraction since the 2008 global financial crisis in Q1 of 2020. The Office for National Statistics (ONS) reported a 2% fall in GDP over the period. A much steeper decline in Q2 could be expected to reflect the nationwide lockdown through April and May.

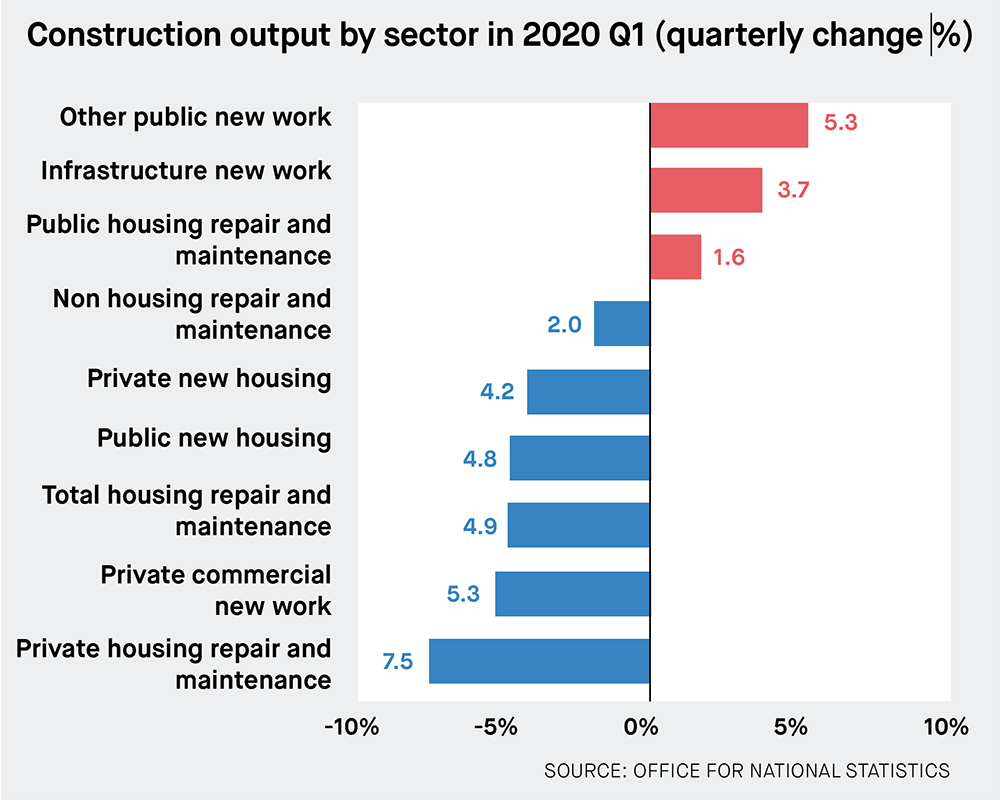

As anticipated, the data shows that construction was badly hit, with output dropping by 2.6% during the quarter, and by 3% quarter-on-year. Just three sectors posted positive growth, with falls driven mainly by the slowing of housebuilding and residential repair and maintenance work.

Infrastructure, however, increased by 3.7% in Q1. Continued infrastructure spend, fuelled by government commitment to key projects, also saw new orders rising by 77.7% in Q1.

New order data is notoriously volatile, and these movements don’t therefore necessarily predicate a trend. However, a healthy pipeline of national and regional infrastructure programmes could provide a crucial bright spot for construction as it weathers the storm.

With recession more of an inevitability than a possibility, thoughts are now turning towards recovery as lockdown measures are eased across England.

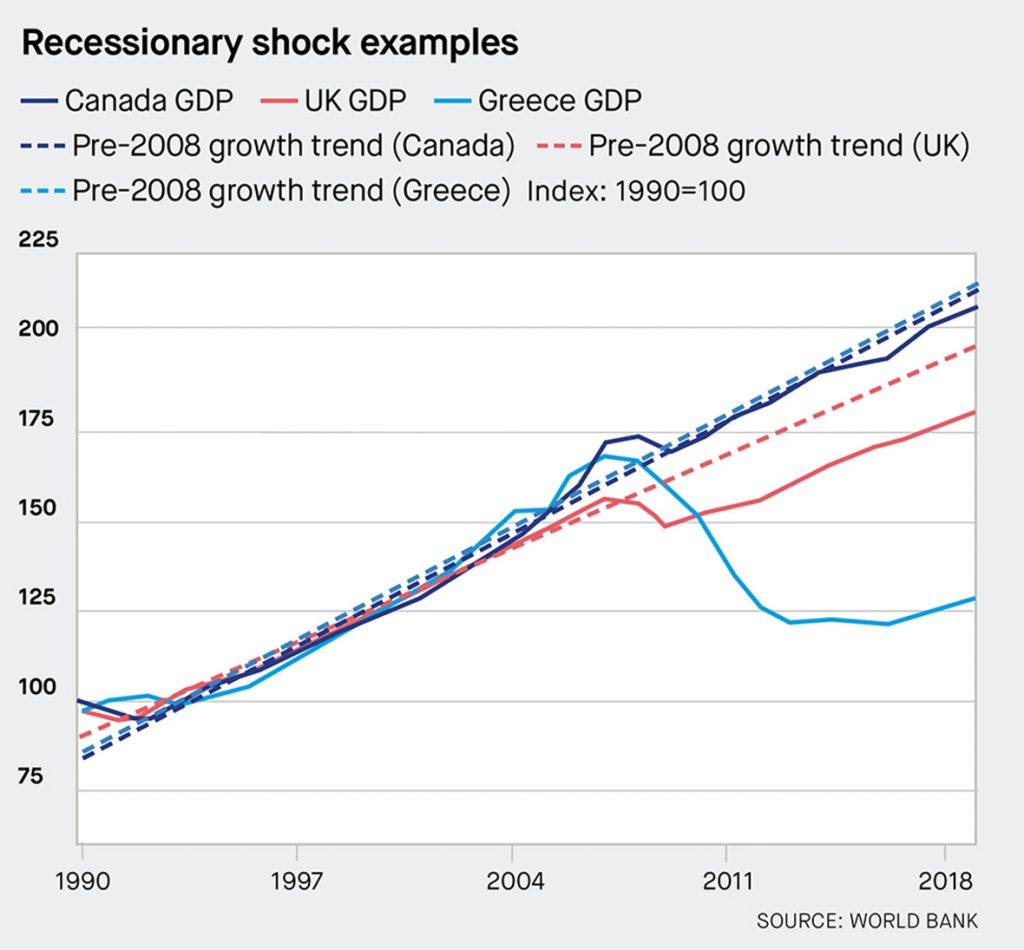

During the 2008 crash we saw a demand-led, ‘balance sheet’ recession. As asset prices fell, economies switched from investment to paying down debt. This triggered a sharp fall in output.

The impact was significant, yet recession and recovery were not mirrored equally across economies.

Canada avoided a banking crisis, meaning less disruption to capital investment. This kept employment high, helping growth return to pre-2008 trends – a ‘V’ shape recession.

An enduring credit crunch saw UK growth fall. Following recovery, growth now runs parallel to pre-crash trends, at a lower level – a ‘U’ shape recession.

Greece never recovered; its growth rate deteriorated and the output gap is widening – an ‘L’ shape recession.

Currently, the Bank of England expects a V-shaped recession in the UK. While welcome, a sharp bounce back would not be without concern for the construction industry.

Rapidly accelerating growth, coupled with restraints on supply chain capacity and capability would impact cost and programmes adversely.

The probability, however, is that we’re caught between a V-shape and a U-shape, producing at a lower threshold to keep people safe, and making a rapid return less likely. One thing that is certain is that the further we move away from a V-shape towards an L-shape, the more construction firms would need to brace for weakening demand.

Kris Hudson is an economist and associate director at Turner & Townsend

Image: Nikita Burukhin/Dreamstime.com