Construction activity accelerated at its fastest rate in nearly five years in July, according to a survey of construction buyers.

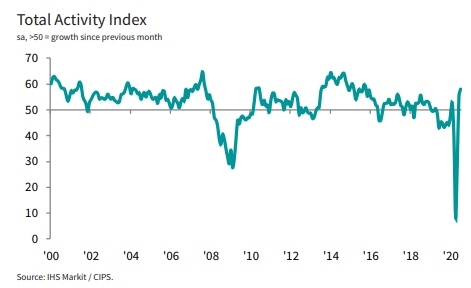

The IHS Markit/CIPS UK Construction Total Activity Index reported a strong expansion of business activity last month, recording a score of 58.1 (where 50.0 indicates no change).

That was up from 55.3 in June, as the construction industry continued its return to work following the coronavirus lockdown.

The main driver of activity in July was residential building, with activity increasing to the greatest extent since September 2014 as buyers reported the release of pent-up demand and reduced anxiety among clients.

Commercial work and civil engineering both also expanded at slightly quicker rates than in June, with the growth often attributed to the catch-up of work that had been delayed, according to respondents.

Meanwhile, the survey found that new orders rose at their fastest rate since February, although the rate of expansion remained softer than that recorded for output levels.

And construction firms were optimistic overall about the prospect of a recovery in business activity during the next 12 months. Around 43% of the survey period expected a rise in output over the coming year, while only 30% forecast a fall.

Nonetheless, the rate at which companies shed jobs increased, with one in three respondents (34%) reporting a fall in employment.

Input cost inflation reached its highest level since May 2019, with pressure on costs partly linked to stretched supply chains.

Tim Moore, economics director at IHS Markit, which compiles the survey said: “Construction companies took another stride along the path to recovery in July as a rebound in house building helped to deliver the strongest overall growth across the sector for nearly five years. Civil engineering and commercial activity are also back in expansion, which has been mainly due to the restart of work that had been delayed during the second quarter of 2020.

“Survey respondents noted a boost to sales from easing lockdown measures across the UK economy and reduced anxiety about starting new projects. However, new work was still relatively thin on the ground, especially outside of residential work, with order book growth much weaker than the rebound in construction output volumes.

“Concerns about the pipeline of new work across the construction sector and intense pressure on margins go a long way to explain the sharp and accelerated fall in employment numbers reported during July. This shortfall of demand was mirrored by the fastest rise in sub-contractor availability since November 2010 and another decline in hourly rates charged.”