Adopting a strategic approach and remaining adaptable will help construction navigate an evolving challenging landscape ahead, writes Pablo Cristi Worm.

In 2024, the construction industry showed resilience, particularly in the second half of the year, as political uncertainties began to dissipate. Although planning reforms and the infrastructure strategy had not yet been announced, the general election in July, followed by the first Labour budget in 14 years in October, contributed to this sense of stability, improving market sentiment compared with 2023.

According to the S&P Global UK Construction PMI, confidence levels are notably higher than a year ago, although there are lingering concerns about future public sector and infrastructure investments. Meanwhile, the RIBA Future Trends Workload Index remains modestly positive, with architects expecting increased workloads.

Economic stability is also helping to stimulate a recovery in private sector investment. With consumer price inflation increasing around the Bank of England’s target, further interest rate cuts are expected in 2025.

However, while the Bank of England appears to have demand-pull inflation, driven by consumer and services prices, under control, cost-push inflation – the increase in the cost of production – remains high and is challenging to control due to its global nature.

A challenging environment

Strengthening domestic demand may further intensify inflationary pressures, especially as supply-side capacity remains constrained in the short term and largely affected by insolvencies in the industry.

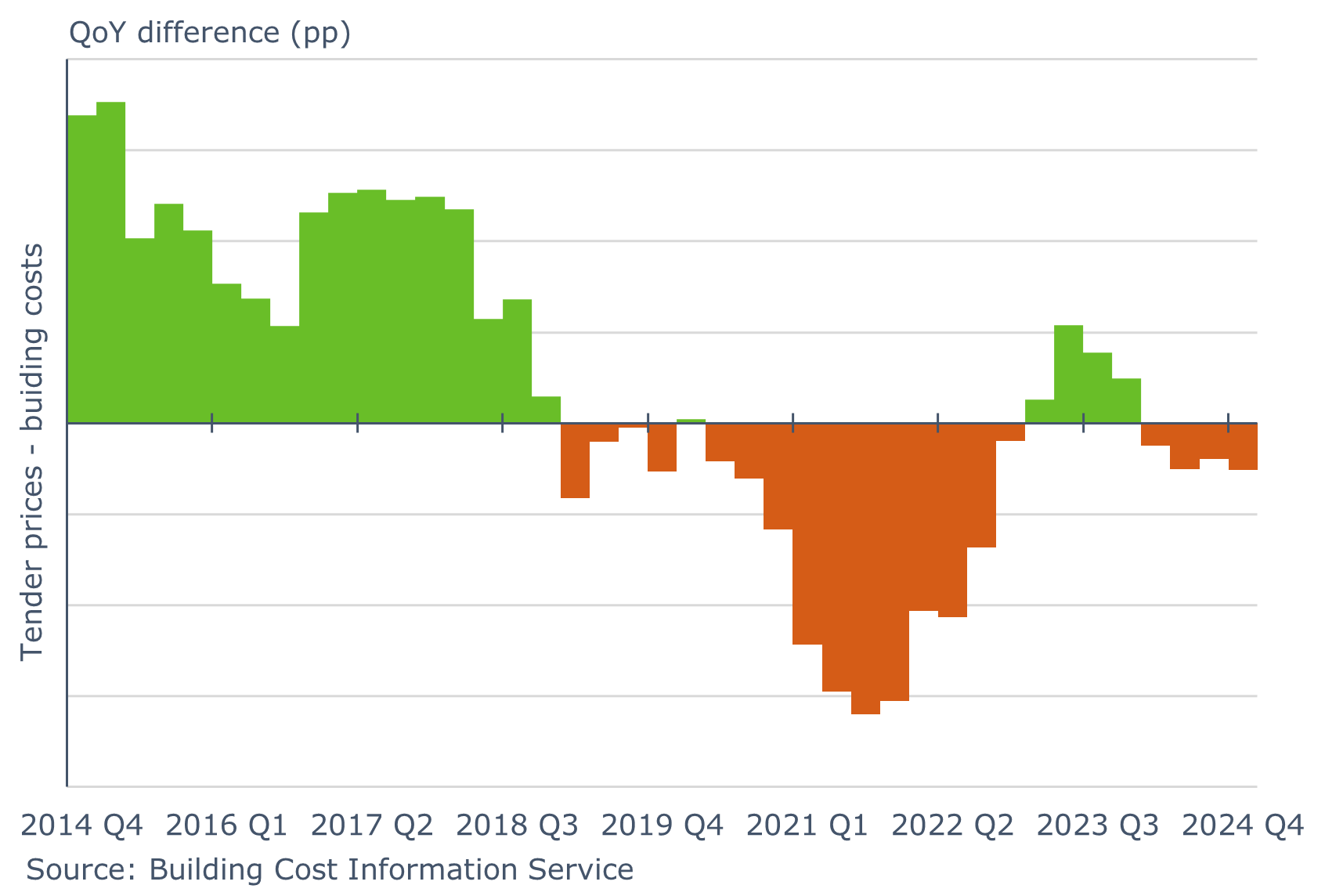

Construction cost escalation has been increasing at a faster pace than tender price inflation (figure 1), placing margins under pressure for an extended period across the supply chain.

Figure 1: difference in the growth rate of tender prices and building costs

It is a challenging environment for contractors, with growing pressure on already limited margins. Profit margins for individual projects across the UK range from 3% to 6%, yet financial reports reveal that some businesses earn significantly less on average.

In 2023, prices briefly increased faster than construction costs, but this trend reversed in 2024. Costs began to outpace prices again, putting sustained pressure on margins despite the short recovery.

Materials prices broadly stabilised in 2024, yet variation exists across different products (figure 2). Cement and concrete products, along with timber and joinery items, are generally slightly above the cumulative levels of last year. In contrast, aggregates, metal and plastic products are, on average, below the cumulative levels of 2023. These prices continue to exhibit fluctuations monthly, reflecting the ongoing volatility in global commodity markets and the supply chain.

Figure 2: construction building materials by composition group, index (2015=100)

Preparing for 2025

Geopolitical risk has heightened with Donald Trump’s election as president of the United States. The prospects of potential confrontation over Taiwan and the South China Sea remain a medium to long-term risk with potentially severe global economic consequences.

The US’s involvement in the Russia-Ukraine conflict and the increasing frequency of joint exercises between China and Russia further amplify geopolitical risks. The ongoing decoupling between the US and China in the technology sector adds another layer of complexity to the global economic outlook.

In the UK, the true impact of the October budget remains to be seen, with the upcoming national infrastructure strategy offering more clarity. The government faces the challenge of balancing tax increases with public spending to maintain economic growth while the Bank of England has warned of higher-than-expected inflation due to the budget measures.

Looking ahead, stakeholders in the construction industry should adopt a proactive and strategic approach to navigate the evolving landscape. Staying informed on economic developments, policy changes, and geopolitical risks will be crucial for future planning. Building strong relationships with suppliers and embracing digital tools can help mitigate uncertainties and optimise resource allocation.

It is essential to remain adaptable, balancing caution with the ability to seize emerging opportunities. By doing so, businesses can better position themselves to weather short-term challenges and capitalise on long-term growth prospects as economic conditions continue to unfold.

Pablo Cristi Worm is an associate economist at Turner & Townsend.