Nitesh Patel explains how fluctuating wages and construction’s acute skills shortage impact the price of materials.

Construction professionals are all familiar with the key cost drivers for their projects: materials, labour and plant. These elements also determine our tender price inflation (TPI) forecasts. This process includes assessing the relationship between falling materials prices on one hand and persistent wage inflation on the other.

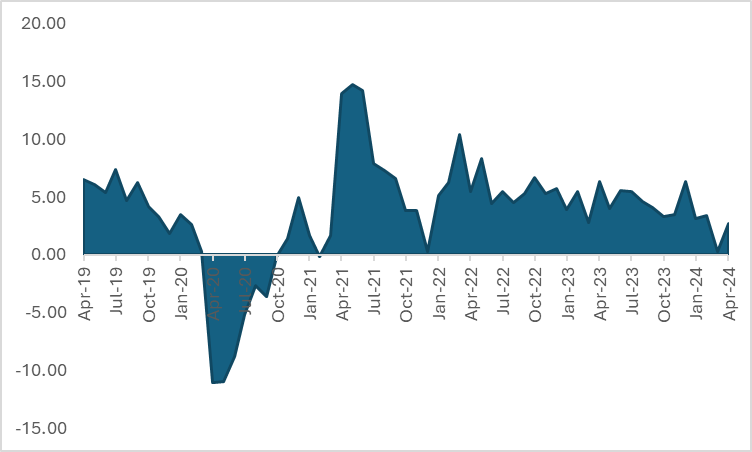

Based on the Department for Business and Trade’s data, the ‘All Work’ materials price index fell by 3.1% in the year to April 2024. This follows the 2.3% fall recorded in March. On this measure, materials prices have been contracting since June 2023. This is a welcome relief to the sector after a peak rate of 26.8% in June 2022 when TPI forecasts were 9.5%.

The fall in energy prices and softening of overall construction demand are contributing to the recent trends in falling materials prices. Price falls for several key building materials were recorded in the year to Q1 2024, the largest being concrete reinforcing bars and structural steel.

Green skills shortage

While these materials price falls will be welcome news to many businesses, Turner & Townsend’s 2024 TPI forecast is down from 3.2% for Q1 to 3%. Fluctuating wages are a key factor in this trend.

In the three months to April 2024, annual wage growth in construction grew to 2.7%, up from 0.3% in March. In December 2023, annual wage growth reached a peak of 6.4%.

Although construction demand has softened, the industry shortage of skilled workers remains acute, and that continues to fuel wage inflation.

-3.1%: material price inflation rate in the year to April 2024

(Source: Department for Business and Trade’s ‘All Work’ material price index)

As Turner & Townsend’s recent International Construction Market Survey 2024 reveals, this impact is particularly significant for green skills, where costs for insulation specialists and solar and heat pump installers in London, for example, have increased by 22% in the past 12 months. This rise threatens the economic viability of sustainable projects, and perhaps the UK’s net-zero ambitions.

Several factors sit behind the general wage increase. The UK’s position outside of the European Union means it cannot attract skilled workers from the European market in the way that it used to. This is combined with an ageing workforce and ongoing difficulties attracting new younger workers. These are not problems with easy solutions, so there is no indication that the upward pressure from wage growth will ease in the foreseeable future.

Building resilience

More positively, construction plant cost inflation rates have eased considerably since May 2022 when they peaked at a record 38.5%, compared with a year earlier. According to the Building Cost and Information Service, the plant cost index has slowed to 5.3% in February 2024, compared with February 2023.

The uncertainty generated by inflation has a direct impact on cost plans, eating into margins, causing misallocation of risk and delaying investment decisions. However, there are some ways to address the inflation risk. First, firms can apply sensitivity analysis to assess impacts on their plans. Another option is to manage risk by looking at alternatives to fixed-price contracts – for example, by combining a guaranteed maximum price with a target cost agreement with incentives to achieve savings.

It is also important to continually revisit the supply chain to test its resilience against both price increases and delays.

Nitesh Patel is a lead economist at Turner & Townsend.