Covid-19’s impact on global supply chains means lengthening lead-in times for many construction products, explains Kris Hudson.

As the daily rates of new covid-19 cases in the UK have dropped, construction has returned to work. When CM went to press, some 97% of Build UK members’ sites were operational again. However, with the pandemic disrupting supply chains both domestically and internationally, many of these sites are now competing for scarce resources.

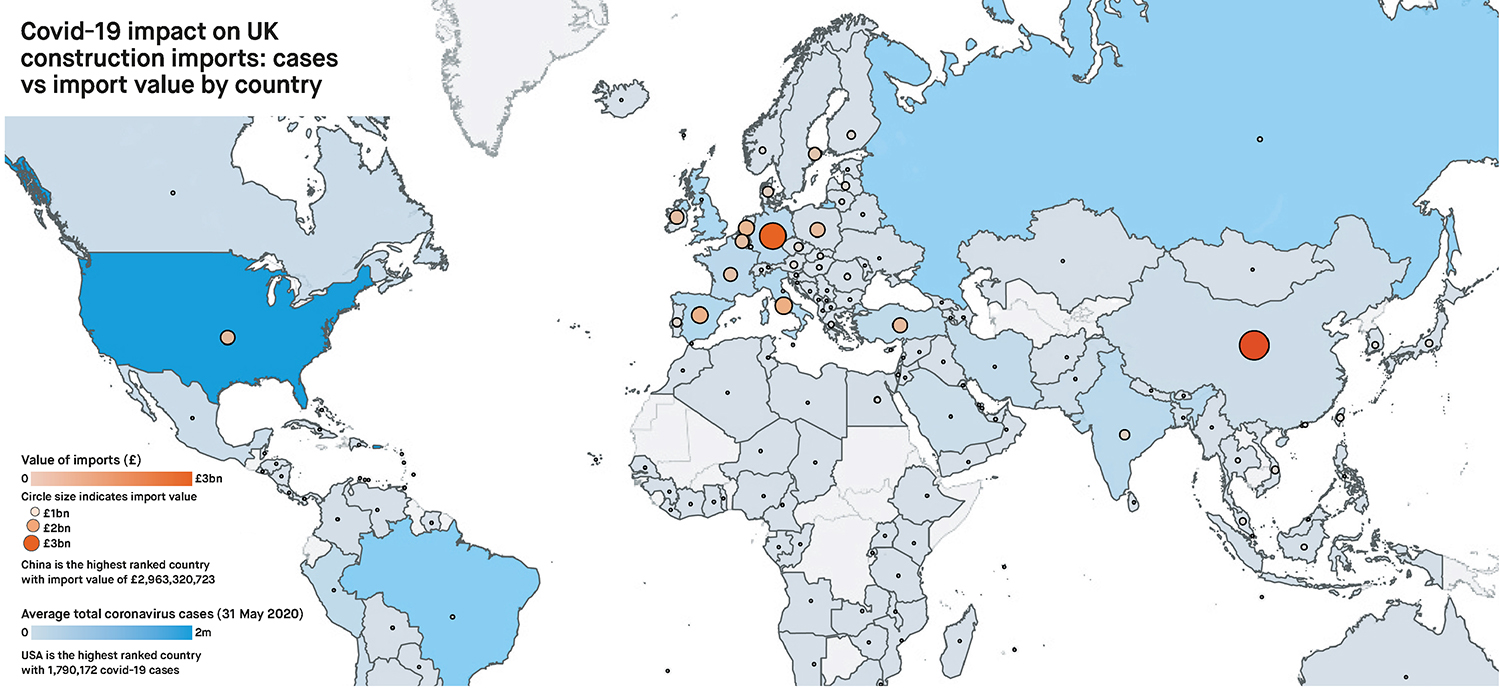

Last year, 46% – or £8.15bn – of all UK imports of construction materials and components came from just five countries: China, Germany, Italy, Spain and the Netherlands.

Spain, Italy and Germany are currently still in the top 10 of countries affected by covid-19 around the world – putting a strain on supply chains. The past months of stringent lockdown have resulted in falling component production in these locations, and the knock-on effect for UK contractors has been lengthening lead-in times for materials, programme delays and higher costs.

Furniture, fixtures and equipment (FF&E), mechanical, electrical and plumbing (MEP) plant, specialist lighting and IT equipment have all been particularly affected, with many global locations seeing eight or nine week delays to lead-in times.

But domestic production of construction material and component is also a concern. The Construction Products Association (CPA) reports that 78% of all construction products are produced in the UK.

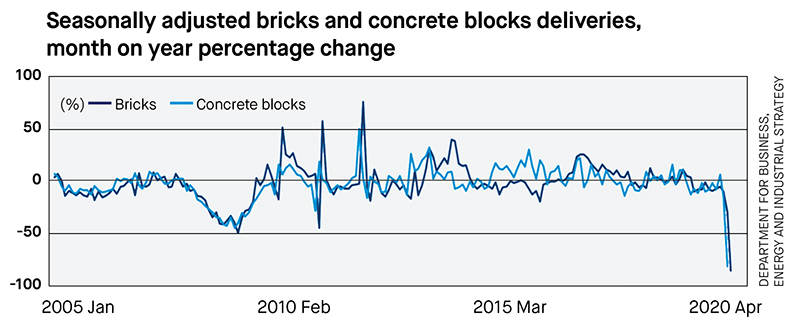

And here the impact of the virus has been particularly stark on the delivery of bricks and blocks. The Department for Business, Energy and Industrial Strategy (BEIS) reports there was an 86.4% decrease in brick deliveries in April 2020 compared to April 2019, with concrete blocks seeing an 81.8% fall over the same period.

The industry may need to brace for further production pressures and longer lead-in times, as suppliers battle with cash flow challenges and insolvencies. The UK’s largest brickmaker, Ibstock, has already reported that it has begun redundancy consultations with 15% of its workforce.

It is clear that contractors, more than ever, need to apply scrutiny and due diligence to the critical path dependency of the goods, components and materials they are sourcing and their condition at the point of transaction.

Planning ahead, analysing and mapping alternatives and proactive supplier engagement will be crucial in understanding and mitigating against any delays or further restrictions in the market.

Kris Hudson is an economist and associate director at Turner & Townsend